Official websites use .gov

A .gov website belongs to an official government organization in the United States.

Secure .gov websites use HTTPS

A lock (

) or https:// means you’ve safely connected to the .gov website. Share sensitive information only on official, secure websites.

Manufacturing Innovation Blog

Powered by the Manufacturing Extension Partnership

Caution: Although the following narrative is about the fabricated metal product manufacturing sector, the story and the statistics themselves have not been fabricated.

Fabricated metal product manufacturing is an important sector to NIST-MEP, and the U.S. economy. The industry sector, which is categorized under the North American Industry Classification System (NAICS) 332, converts metal into intermediate and end-use products by assembling, bending, forging, forming, machining, stamping, and welding [1].

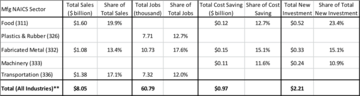

The sector accounts for the lion’s share of MEP’s clientele and survey impacts. During the calendar years (CY) 2010-2012, the sector’s shares in total MEP survey impacts ranked (See Table 1) in the top three for sales, jobs, cost saving, and new investment impacts. In CY 2012 for instance, the sector [2] accounted for 13 percent of a total MEP-wide sales impact of $8 billion, the third largest share among all 3-digit manufacturing NAICS sectors. Fabricated metal clients also accounted for 18 percent of the nearly 61,000 total direct job impacts, the largest share among all manufacturing subsectors. The sector’s share in total MEP cost-saving impact of $966 million was 15 percent, the largest fraction among all the sectors. Out of a total MEP new-investment impact of $2.2 billion across all sectors, fabricated metal product manufacturing accounted for 15 percent of the impacts, the second largest.

** Totals include all 3-digit manufacturing NAICS code sectors plus R&D, and are, therefore, more than the aggregate for the individual sector impacts listed in the table.

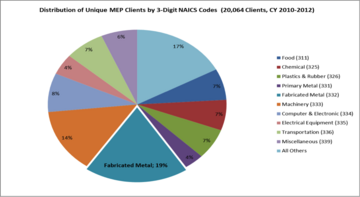

With MEP serving an annual average of 6,687 unique manufacturing clients during the CY period 2010-2012, the fabricated metal product manufacturing sector accounted for 19 percent of MEP clients (see Chart 1), the highest single share among all 3-digits manufacturing NAICS (311—339), followed by the machinery manufacturing sector (14 percent).

However, the dominance of the fabricated metal product manufacturing impacts is not limited to MEP only. The sector contributed $137.8 billion (7.4 percent share) in real manufacturing gross domestic product (GDP) in CY 2012, up 2 percent from the previous year, and representing fifth largest share in manufacturing GDP. After declining 24 percent to $118 billion in 2009 due to the recession, fabricated metal product manufacturing sector has mostly recovered, recording a 5.4-percent average growth during the period 2010 and 2012. The sector also generated $44.6 billion (see Chart 2) in export earnings in 2012, with the bulk of the shipments (47 percent) going to NAFTA partners, Mexico and Canada. Nearly $1.8 billion, $1.7 billion, and $1.3 billion of the sector’s 2012 exports went to China, the United Kingdom, and Japan, respectively.

Nationwide there are about 58,000 manufacturing establishments in the sector, accounting for 1.4 million (13 percent) of the 10.5 million total direct manufacturing jobs in CY 2012. The average annual earnings per employee in the sector currently stand at $64,000. The only other sectors with larger shares of manufacturing employment are the food and transportation equipment manufacturing sectors, each with 13 percent of total direct manufacturing jobs. The fabricated metal product manufacturing sector’s employment location quotients (LQs)—which are summary measures of an industry’s regional importance—show that the sector is more concentrated in the States of Wisconsin, Ohio, Indiana, and Michigan (with 2012 LQs of 2.5, 1.9, 1.8, and 1.8, respectively).

Going forward, challenges, as well as opportunities remain. In surveys of MEP clients, fabricated metal manufacturers cite cost reduction, finding growth opportunities, and employee recruitment as top three challenges they face in the near future. It is, therefore, not surprising that those same clients disproportionately cite staff expertise and cost of services as reasons for choosing MEP Center services. By several indicators, fabricated metal product manufacturing sector is the fastest growing in this industry. MEP Centers can therefore expect to continue to harness their expertise and competitive service costs to attract more sector clients with the aim of minimizing production costs and supply chain bottlenecks, and ultimately creating more American jobs and improving the quality of life.

About the author

Related Posts

Comments

- Reply